The effects of Brexit#

The aim of this notebook is to estimate the causal impact of Brexit upon the UK’s GDP. This will be done using the synthetic control approach. As such, it is similar to the policy brief “What can we know about the cost of Brexit so far?” [Springford, 2022] from the Center for European Reform. That approach did not use Bayesian estimation methods however.

I did not use the GDP data from the above report however as it had been scaled in some way that was hard for me to understand how it related to the absolute GDP figures. Instead, GDP data was obtained courtesy of Prof. Dooruj Rambaccussing. Raw data is in units of trillions of USD.

import arviz as az

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import seaborn as sns

from pymc_extras.prior import Prior

import causalpy as cp

%load_ext autoreload

%autoreload 2

%config InlineBackend.figure_format = 'retina'

seed = 42

Load data#

df = (

cp.load_data("brexit")

.assign(Time=lambda x: pd.to_datetime(x["Time"]))

.set_index("Time")

.loc[lambda x: x.index >= "2009-01-01"]

# manual exclusion of some countries

.drop(["Japan", "Italy", "US", "Spain", "Portugal"], axis=1)

)

# specify date of the Brexit vote announcement

treatment_time = pd.to_datetime("2016 June 24")

df.head()

| Australia | Austria | Belgium | Canada | Denmark | Finland | France | Germany | Iceland | Luxemburg | Netherlands | New_Zealand | Norway | Sweden | Switzerland | UK | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Time | ||||||||||||||||

| 2009-01-01 | 3.84048 | 0.802836 | 0.94117 | 16.93824 | 4.50096 | 0.51052 | 5.05450 | 6.63471 | 5.18157 | 0.114836 | 1.634391 | 0.47336 | 7.78753 | 10.32220 | 1.476532 | 4.61881 |

| 2009-04-01 | 3.86954 | 0.796545 | 0.94162 | 16.75340 | 4.41372 | 0.50829 | 5.05375 | 6.64530 | 5.16171 | 0.116259 | 1.634432 | 0.47916 | 7.71903 | 10.32867 | 1.485509 | 4.60431 |

| 2009-07-01 | 3.88115 | 0.799937 | 0.95352 | 16.82878 | 4.42898 | 0.51299 | 5.06237 | 6.68237 | 5.24132 | 0.118747 | 1.640982 | 0.48188 | 7.72400 | 10.32328 | 1.502506 | 4.60722 |

| 2009-10-01 | 3.91028 | 0.803823 | 0.96117 | 17.02503 | 4.43300 | 0.50903 | 5.09832 | 6.73155 | 5.22482 | 0.119302 | 1.650866 | 0.48805 | 7.72812 | 10.37107 | 1.515139 | 4.62152 |

| 2010-01-01 | 3.92716 | 0.800510 | 0.96615 | 17.23041 | 4.47128 | 0.51413 | 5.11625 | 6.78621 | 4.91128 | 0.121414 | 1.647748 | 0.49349 | 7.87891 | 10.64833 | 1.525864 | 4.65380 |

# get useful country lists

target_country = "UK"

all_countries = df.columns

other_countries = all_countries.difference({target_country})

all_countries = list(all_countries)

other_countries = list(other_countries)

Data visualization#

az.style.use("arviz-white")

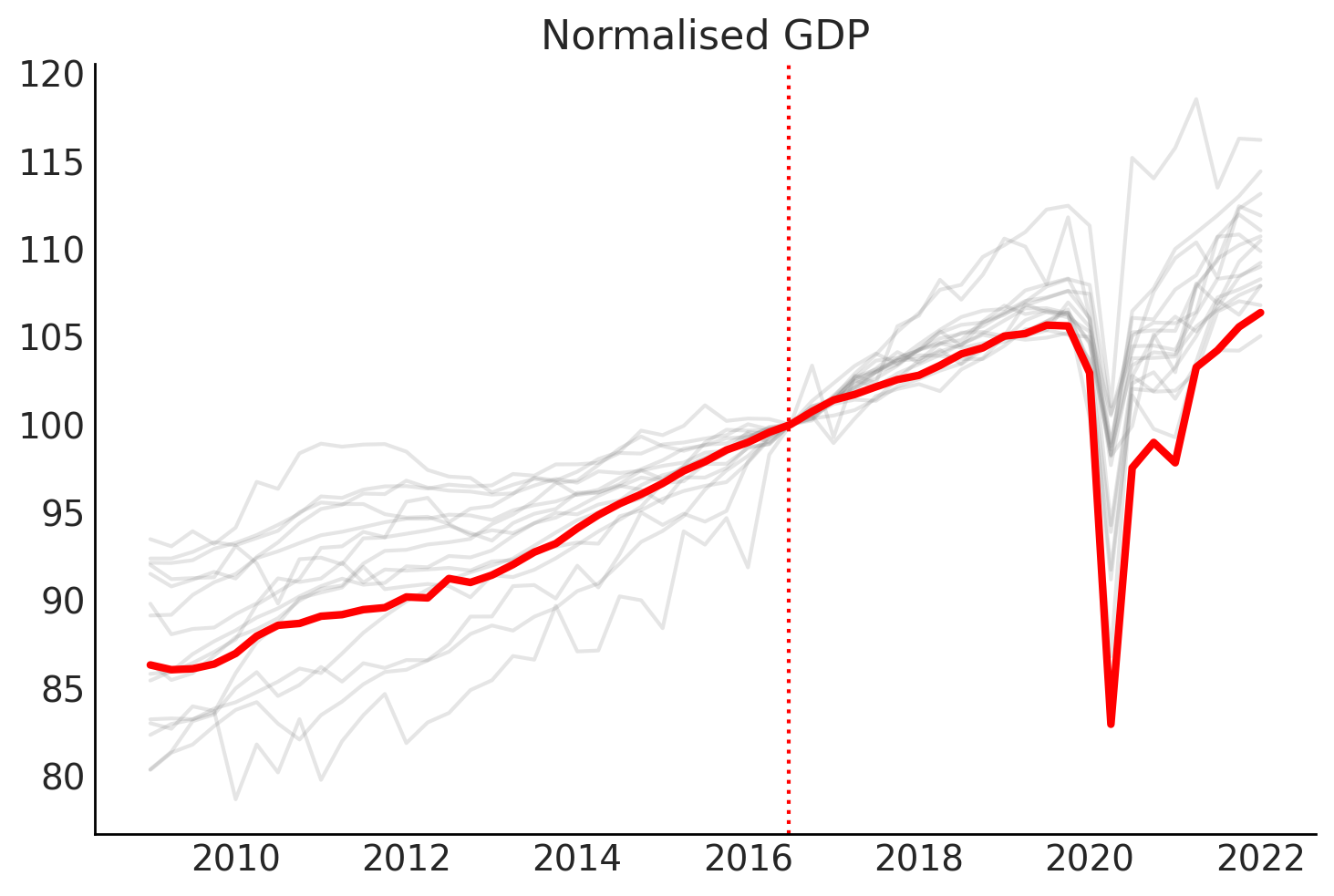

# Plot the time series normalised so that intervention point (Q3 2016) is equal to 100

gdp_at_intervention = df.loc[pd.to_datetime("2016 July 01"), :]

df_normalised = (df / gdp_at_intervention) * 100.0

# plot

fig, ax = plt.subplots()

for col in other_countries:

ax.plot(df_normalised.index, df_normalised[col], color="grey", alpha=0.2)

ax.plot(df_normalised.index, df_normalised[target_country], color="red", lw=3)

# ax = df_normalised.plot(legend=False)

# formatting

ax.set(title="Normalised GDP")

ax.axvline(x=treatment_time, color="r", ls=":");

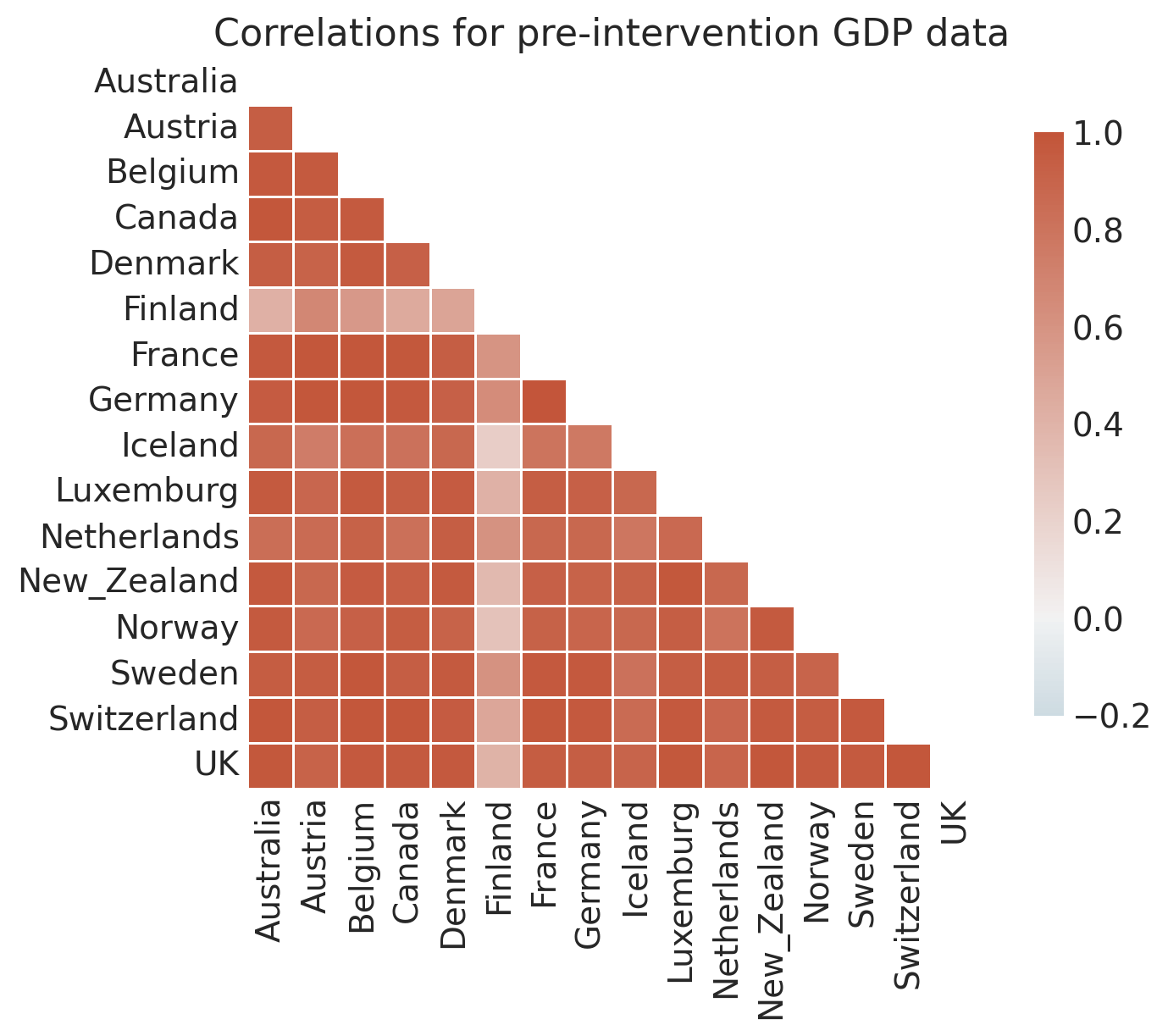

# Examine how correlated the pre-intervention time series are

pre_intervention_data = df.loc[df.index < treatment_time, :]

corr = pre_intervention_data.corr()

f, ax = plt.subplots(figsize=(8, 6))

ax = sns.heatmap(

corr,

mask=np.triu(np.ones_like(corr, dtype=bool)),

cmap=sns.diverging_palette(230, 20, as_cmap=True),

vmin=-0.2,

vmax=1.0,

center=0,

square=True,

linewidths=0.5,

cbar_kws={"shrink": 0.8},

)

ax.set(title="Correlations for pre-intervention GDP data");

Run the analysis#

Note: The analysis is (and should be) run on the raw GDP data. We do not use the normalised data shown above which was just for ease of visualization.

Note

The random_seed keyword argument for the PyMC sampler is not necessary. We use it here so that the results are reproducible.

sample_kwargs = {"tune": 1000, "target_accept": 0.99, "random_seed": seed}

result = cp.SyntheticControl(

df,

treatment_time,

control_units=other_countries,

treated_units=[target_country],

model=cp.pymc_models.WeightedSumFitter(

sample_kwargs=sample_kwargs,

),

)

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (4 chains in 4 jobs)

NUTS: [beta, y_hat_sigma]

Sampling 4 chains for 1_000 tune and 1_000 draw iterations (4_000 + 4_000 draws total) took 70 seconds.

There were 1 divergences after tuning. Increase `target_accept` or reparameterize.

Chain 0 reached the maximum tree depth. Increase `max_treedepth`, increase `target_accept` or reparameterize.

Chain 1 reached the maximum tree depth. Increase `max_treedepth`, increase `target_accept` or reparameterize.

Chain 2 reached the maximum tree depth. Increase `max_treedepth`, increase `target_accept` or reparameterize.

Chain 3 reached the maximum tree depth. Increase `max_treedepth`, increase `target_accept` or reparameterize.

The rhat statistic is larger than 1.01 for some parameters. This indicates problems during sampling. See https://arxiv.org/abs/1903.08008 for details

Sampling: [beta, y_hat, y_hat_sigma]

Sampling: [y_hat]

Sampling: [y_hat]

Sampling: [y_hat]

Sampling: [y_hat]

While we are at it, let’s plot the graphviz representation of the model. This shows us the inner workings of the WeightedSumFitter class which defines our synthetic control model with a sum to 1 constraint on the donor weights (here labelled as coeffs). This will be particularly useful when we come to exploring custom priors (see below).

result.model.to_graphviz()

We currently get some divergences, but these are mostly dealt with by increasing tune and target_accept sampling parameters. Nevertheless, the sampling of this dataset/model combination feels a little brittle.

result.idata

-

<xarray.Dataset> Size: 1MB Dimensions: (chain: 4, draw: 1000, treated_units: 1, coeffs: 15, obs_ind: 30) Coordinates: * chain (chain) int64 32B 0 1 2 3 * draw (draw) int64 8kB 0 1 2 3 4 5 6 ... 994 995 996 997 998 999 * treated_units (treated_units) <U2 8B 'UK' * coeffs (coeffs) <U11 660B 'Australia' 'Austria' ... 'Switzerland' * obs_ind (obs_ind) int64 240B 0 1 2 3 4 5 6 7 ... 23 24 25 26 27 28 29 Data variables: beta (chain, draw, treated_units, coeffs) float64 480kB 0.2496 ... y_hat_sigma (chain, draw, treated_units) float64 32kB 0.02687 ... 0.03445 mu (chain, draw, obs_ind, treated_units) float64 960kB 4.608 ... Attributes: created_at: 2025-11-14T11:13:28.926299+00:00 arviz_version: 0.21.0 inference_library: pymc inference_library_version: 5.23.0 sampling_time: 69.69903612136841 tuning_steps: 1000 -

<xarray.Dataset> Size: 968kB Dimensions: (chain: 4, draw: 1000, obs_ind: 30, treated_units: 1) Coordinates: * chain (chain) int64 32B 0 1 2 3 * draw (draw) int64 8kB 0 1 2 3 4 5 6 ... 994 995 996 997 998 999 * obs_ind (obs_ind) int64 240B 0 1 2 3 4 5 6 7 ... 23 24 25 26 27 28 29 * treated_units (treated_units) <U2 8B 'UK' Data variables: y_hat (chain, draw, obs_ind, treated_units) float64 960kB 4.62 .... Attributes: created_at: 2025-11-14T11:13:29.143734+00:00 arviz_version: 0.21.0 inference_library: pymc inference_library_version: 5.23.0 -

<xarray.Dataset> Size: 496kB Dimensions: (chain: 4, draw: 1000) Coordinates: * chain (chain) int64 32B 0 1 2 3 * draw (draw) int64 8kB 0 1 2 3 4 5 ... 995 996 997 998 999 Data variables: (12/17) acceptance_rate (chain, draw) float64 32kB 0.9909 0.9988 ... 0.9941 step_size_bar (chain, draw) float64 32kB 0.001979 ... 0.001812 step_size (chain, draw) float64 32kB 0.00164 ... 0.002034 energy_error (chain, draw) float64 32kB 0.02131 ... -0.08462 n_steps (chain, draw) float64 32kB 1.023e+03 ... 1.023e+03 process_time_diff (chain, draw) float64 32kB 0.03708 ... 0.03781 ... ... perf_counter_diff (chain, draw) float64 32kB 0.03715 ... 0.03786 diverging (chain, draw) bool 4kB False False ... False False largest_eigval (chain, draw) float64 32kB nan nan nan ... nan nan energy (chain, draw) float64 32kB -28.81 -25.42 ... -31.29 reached_max_treedepth (chain, draw) bool 4kB True True True ... True False lp (chain, draw) float64 32kB 32.78 39.79 ... 35.35 Attributes: created_at: 2025-11-14T11:13:28.932843+00:00 arviz_version: 0.21.0 inference_library: pymc inference_library_version: 5.23.0 sampling_time: 69.69903612136841 tuning_steps: 1000 -

<xarray.Dataset> Size: 189kB Dimensions: (chain: 1, draw: 500, treated_units: 1, coeffs: 15, obs_ind: 30) Coordinates: * chain (chain) int64 8B 0 * draw (draw) int64 4kB 0 1 2 3 4 5 6 ... 494 495 496 497 498 499 * treated_units (treated_units) <U2 8B 'UK' * coeffs (coeffs) <U11 660B 'Australia' 'Austria' ... 'Switzerland' * obs_ind (obs_ind) int64 240B 0 1 2 3 4 5 6 7 ... 23 24 25 26 27 28 29 Data variables: y_hat_sigma (chain, draw, treated_units) float64 4kB 0.4183 ... 0.9914 beta (chain, draw, treated_units, coeffs) float64 60kB 0.01287 ... mu (chain, draw, obs_ind, treated_units) float64 120kB 5.228 ... Attributes: created_at: 2025-11-14T11:13:29.063859+00:00 arviz_version: 0.21.0 inference_library: pymc inference_library_version: 5.23.0 -

<xarray.Dataset> Size: 124kB Dimensions: (chain: 1, draw: 500, obs_ind: 30, treated_units: 1) Coordinates: * chain (chain) int64 8B 0 * draw (draw) int64 4kB 0 1 2 3 4 5 6 ... 494 495 496 497 498 499 * obs_ind (obs_ind) int64 240B 0 1 2 3 4 5 6 7 ... 23 24 25 26 27 28 29 * treated_units (treated_units) <U2 8B 'UK' Data variables: y_hat (chain, draw, obs_ind, treated_units) float64 120kB 5.753 ... Attributes: created_at: 2025-11-14T11:13:29.065707+00:00 arviz_version: 0.21.0 inference_library: pymc inference_library_version: 5.23.0 -

<xarray.Dataset> Size: 488B Dimensions: (obs_ind: 30, treated_units: 1) Coordinates: * obs_ind (obs_ind) int64 240B 0 1 2 3 4 5 6 7 ... 23 24 25 26 27 28 29 * treated_units (treated_units) <U2 8B 'UK' Data variables: y_hat (obs_ind, treated_units) float64 240B 4.619 4.604 ... 5.327 Attributes: created_at: 2025-11-14T11:13:28.935117+00:00 arviz_version: 0.21.0 inference_library: pymc inference_library_version: 5.23.0 -

<xarray.Dataset> Size: 4kB Dimensions: (obs_ind: 30, coeffs: 15) Coordinates: * obs_ind (obs_ind) int64 240B 0 1 2 3 4 5 6 7 8 ... 22 23 24 25 26 27 28 29 * coeffs (coeffs) <U11 660B 'Australia' 'Austria' ... 'Sweden' 'Switzerland' Data variables: X (obs_ind, coeffs) float64 4kB 3.84 0.8028 0.9412 ... 12.37 1.719 Attributes: created_at: 2025-11-14T11:13:28.936057+00:00 arviz_version: 0.21.0 inference_library: pymc inference_library_version: 5.23.0

Check the MCMC chain mixing via the Rhat statistic.

az.summary(result.idata, var_names=["~mu"])

| mean | sd | hdi_3% | hdi_97% | mcse_mean | mcse_sd | ess_bulk | ess_tail | r_hat | |

|---|---|---|---|---|---|---|---|---|---|

| beta[UK, Australia] | 0.121 | 0.074 | 0.001 | 0.243 | 0.003 | 0.001 | 607.0 | 656.0 | 1.00 |

| beta[UK, Austria] | 0.046 | 0.042 | 0.000 | 0.123 | 0.001 | 0.001 | 808.0 | 703.0 | 1.01 |

| beta[UK, Belgium] | 0.052 | 0.048 | 0.000 | 0.140 | 0.001 | 0.001 | 784.0 | 618.0 | 1.00 |

| beta[UK, Canada] | 0.038 | 0.023 | 0.000 | 0.077 | 0.001 | 0.000 | 472.0 | 476.0 | 1.01 |

| beta[UK, Denmark] | 0.085 | 0.065 | 0.000 | 0.200 | 0.002 | 0.001 | 581.0 | 573.0 | 1.00 |

| beta[UK, Finland] | 0.041 | 0.039 | 0.000 | 0.113 | 0.001 | 0.001 | 873.0 | 935.0 | 1.00 |

| beta[UK, France] | 0.031 | 0.028 | 0.000 | 0.084 | 0.001 | 0.001 | 749.0 | 728.0 | 1.00 |

| beta[UK, Germany] | 0.026 | 0.025 | 0.000 | 0.072 | 0.001 | 0.001 | 680.0 | 897.0 | 1.00 |

| beta[UK, Iceland] | 0.154 | 0.041 | 0.075 | 0.230 | 0.001 | 0.001 | 844.0 | 943.0 | 1.00 |

| beta[UK, Luxemburg] | 0.049 | 0.045 | 0.000 | 0.134 | 0.001 | 0.001 | 738.0 | 553.0 | 1.00 |

| beta[UK, Netherlands] | 0.048 | 0.043 | 0.000 | 0.126 | 0.001 | 0.001 | 996.0 | 995.0 | 1.00 |

| beta[UK, New_Zealand] | 0.062 | 0.055 | 0.000 | 0.164 | 0.002 | 0.001 | 627.0 | 605.0 | 1.00 |

| beta[UK, Norway] | 0.082 | 0.045 | 0.000 | 0.156 | 0.002 | 0.001 | 621.0 | 568.0 | 1.01 |

| beta[UK, Sweden] | 0.100 | 0.031 | 0.043 | 0.160 | 0.001 | 0.001 | 837.0 | 719.0 | 1.01 |

| beta[UK, Switzerland] | 0.065 | 0.057 | 0.000 | 0.172 | 0.001 | 0.001 | 3963.0 | 2199.0 | 1.00 |

| y_hat_sigma[UK] | 0.031 | 0.005 | 0.023 | 0.040 | 0.000 | 0.000 | 1036.0 | 1488.0 | 1.00 |

You can inspect the traces in more detail with:

az.plot_trace(result.idata, var_names="~mu", compact=False);

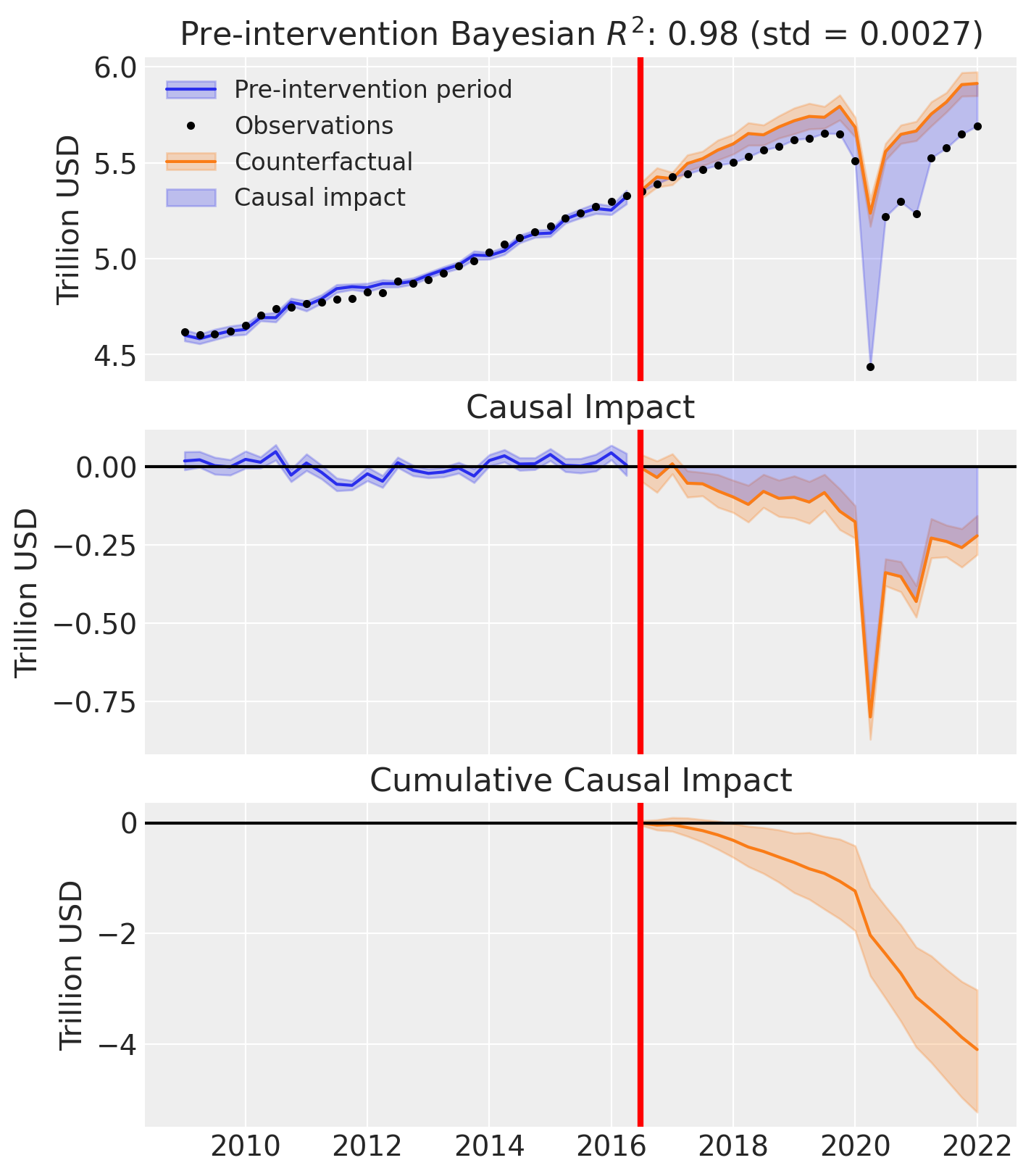

az.style.use("arviz-darkgrid")

fig, ax = result.plot(plot_predictors=False)

for i in [0, 1, 2]:

ax[i].set(ylabel="Trillion USD")

result.summary()

================================SyntheticControl================================

Control units: ['Australia', 'Austria', 'Belgium', 'Canada', 'Denmark', 'Finland', 'France', 'Germany', 'Iceland', 'Luxemburg', 'Netherlands', 'New_Zealand', 'Norway', 'Sweden', 'Switzerland']

Treated unit: UK

Model coefficients:

Australia 0.12, 94% HDI [0.0086, 0.27]

Austria 0.046, 94% HDI [0.0013, 0.15]

Belgium 0.052, 94% HDI [0.0016, 0.17]

Canada 0.038, 94% HDI [0.0025, 0.085]

Denmark 0.085, 94% HDI [0.0031, 0.23]

Finland 0.041, 94% HDI [0.0015, 0.14]

France 0.031, 94% HDI [0.0011, 0.1]

Germany 0.026, 94% HDI [0.00096, 0.086]

Iceland 0.15, 94% HDI [0.075, 0.23]

Luxemburg 0.049, 94% HDI [0.0011, 0.16]

Netherlands 0.048, 94% HDI [0.0021, 0.16]

New_Zealand 0.062, 94% HDI [0.0015, 0.19]

Norway 0.082, 94% HDI [0.0076, 0.17]

Sweden 0.1, 94% HDI [0.039, 0.16]

Switzerland 0.065, 94% HDI [0.0024, 0.2]

y_hat_sigma 0.031, 94% HDI [0.023, 0.041]

Effect Summary Reporting#

For decision-making, you often need a concise summary of the causal effect with key statistics. The effect_summary() method provides a decision-ready report with average and cumulative effects, HDI intervals, tail probabilities, and relative effects. This provides a comprehensive summary without manual post-processing.

# Generate effect summary for the full post-period

stats = result.effect_summary()

stats.table

| mean | median | hdi_lower | hdi_upper | p_gt_0 | relative_mean | relative_hdi_lower | relative_hdi_upper | |

|---|---|---|---|---|---|---|---|---|

| average | -0.178323 | -0.179121 | -0.227586 | -0.127143 | 0.0 | -3.164222 | -4.005843 | -2.278178 |

| cumulative | -4.101438 | -4.119792 | -5.234484 | -2.924293 | 0.0 | -3.164222 | -4.005843 | -2.278178 |

# View the prose summary

print(stats.text)

Post-period (2016-07-01 00:00:00 to 2022-01-01 00:00:00), the average effect was -0.18 (95% HDI [-0.23, -0.13]), with a posterior probability of an increase of 0.000. The cumulative effect was -4.10 (95% HDI [-5.23, -2.92]); probability of an increase 0.000. Relative to the counterfactual, this equals -3.16% on average (95% HDI [-4.01%, -2.28%]).

# You can also analyze a specific time window, e.g., the first year after Brexit

stats_window = result.effect_summary(

window=(pd.to_datetime("2016-06-24"), pd.to_datetime("2017-06-24"))

)

stats_window.table

| mean | median | hdi_lower | hdi_upper | p_gt_0 | relative_mean | relative_hdi_lower | relative_hdi_upper | |

|---|---|---|---|---|---|---|---|---|

| average | -0.021407 | -0.021822 | -0.064357 | 0.021860 | 0.1635 | -0.393064 | -1.17724 | 0.406281 |

| cumulative | -0.085627 | -0.087289 | -0.257429 | 0.087441 | 0.1635 | -0.393064 | -1.17724 | 0.406281 |

Custom priors#

The analysis above is all based upon the default priors for the WeightedSumFitter class. But this might not always be appropriate. In particular the default Priors are Dirichlet distributed with an alpha parameter of 1. This corresponds to a uniform prior over the simplex.

But we might have different prior beliefs. For example, we might think that some control units will play a larger role and some control units will be irrelevant. In which case, we could use as less concentrated prior, such as \(\mathrm{Dirichlet}(0.1)\).

We can do this in the code below.

n_control_units = len(other_countries)

result_custom = cp.SyntheticControl(

df,

treatment_time,

control_units=other_countries,

treated_units=[target_country],

model=cp.pymc_models.WeightedSumFitter(

sample_kwargs=sample_kwargs,

priors={

"beta": Prior(

"Dirichlet",

a=0.1 * np.ones(n_control_units),

dims=["treated_units", "coeffs"],

),

},

),

)

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (4 chains in 4 jobs)

NUTS: [beta, y_hat_sigma]

Sampling 4 chains for 1_000 tune and 1_000 draw iterations (4_000 + 4_000 draws total) took 81 seconds.

There were 168 divergences after tuning. Increase `target_accept` or reparameterize.

Chain 0 reached the maximum tree depth. Increase `max_treedepth`, increase `target_accept` or reparameterize.

Chain 1 reached the maximum tree depth. Increase `max_treedepth`, increase `target_accept` or reparameterize.

Chain 2 reached the maximum tree depth. Increase `max_treedepth`, increase `target_accept` or reparameterize.

Chain 3 reached the maximum tree depth. Increase `max_treedepth`, increase `target_accept` or reparameterize.

The rhat statistic is larger than 1.01 for some parameters. This indicates problems during sampling. See https://arxiv.org/abs/1903.08008 for details

The effective sample size per chain is smaller than 100 for some parameters. A higher number is needed for reliable rhat and ess computation. See https://arxiv.org/abs/1903.08008 for details

Sampling: [beta, y_hat, y_hat_sigma]

Sampling: [y_hat]

Sampling: [y_hat]

Sampling: [y_hat]

Sampling: [y_hat]

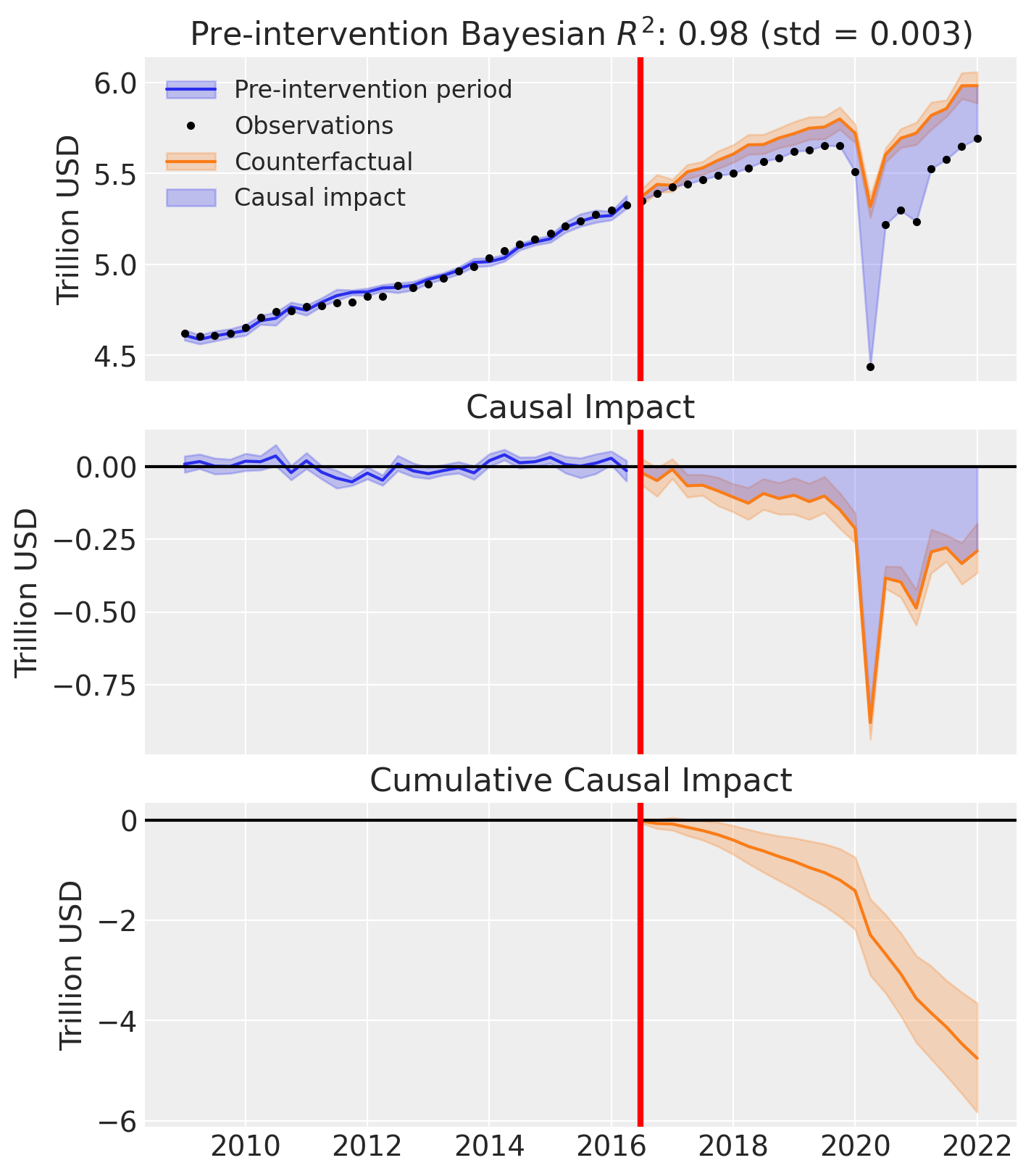

The main results plot shows only minor differences in terms of fitting.

fig, ax = result_custom.plot(plot_predictors=False)

for i in [0, 1, 2]:

ax[i].set(ylabel="Trillion USD")

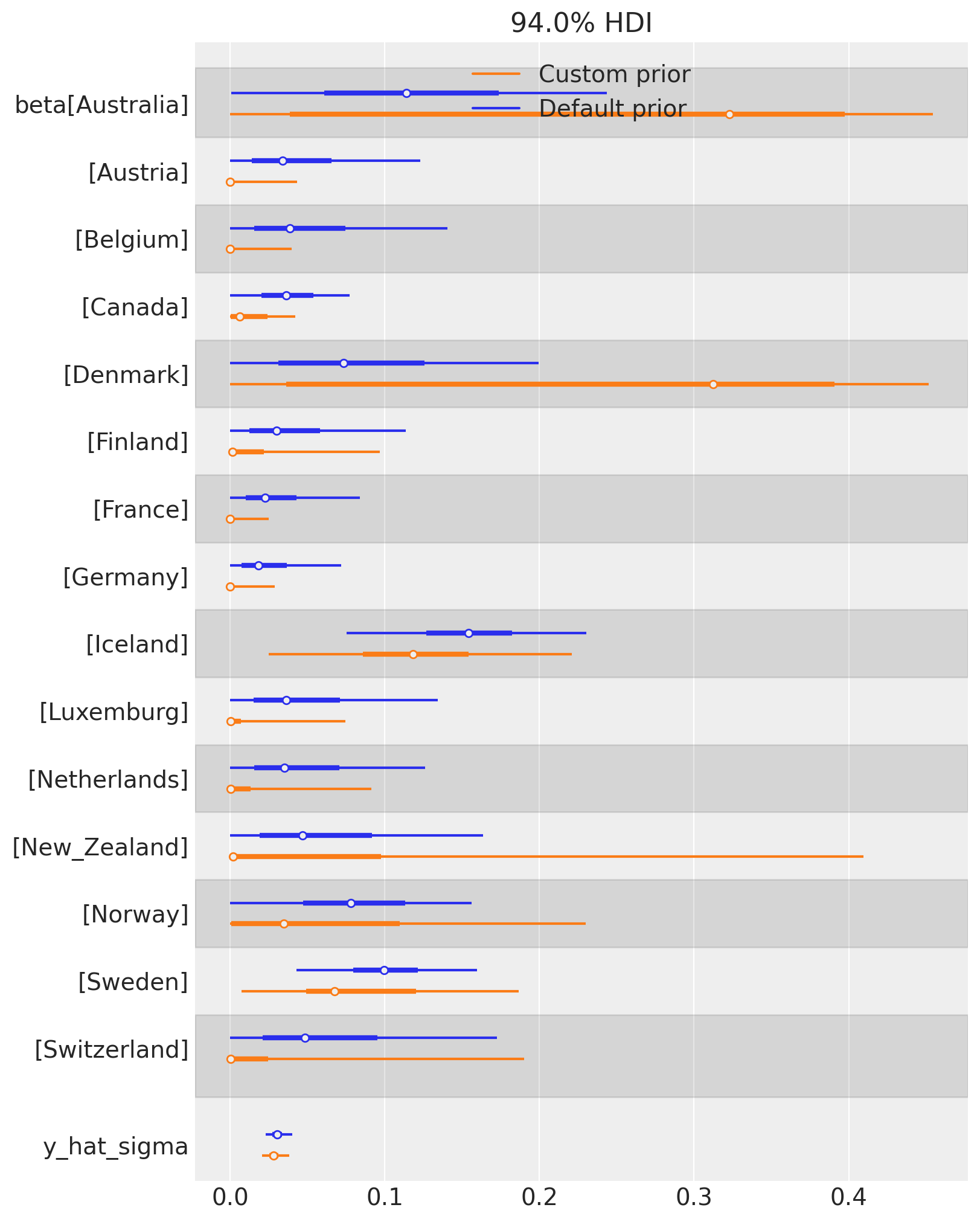

We can also examine the effect of changing the Dirichlet prior on the posterior distribution of weights. TWe can see that the custom prior of \(\mathrm{Dirichlet}(0.1)\) results in more sparse weights over control countries. The posterior of many countries are more concentrated near zero (e.g. Austria, Canada, Germany, etc), while others have increased in importance (e.g. Denmark, and Australia).

This is a rich area for discussion, but the key point is that users can define their own prior beliefs about the weights in the synthetic control model. There are some benefits from having ‘sparsifying’ priors in that they can help identify a smaller set of key control units that are most relevant to constructing the synthetic control.

Show code cell source

az.plot_forest(

[result.idata, result_custom.idata],

model_names=["Default prior", "Custom prior"],

var_names=["beta", "y_hat_sigma"],

combined=True,

figsize=(8, 10),

);

References#

John Springford. What can we know about the cost of brexit so far? 2022. URL: https://www.cer.eu/publications/archive/policy-brief/2022/cost-brexit-so-far.